Diagram

| Super-types: | None |

|---|---|

| Sub-types: | None |

| Name | ProtectionTerms |

|---|---|

| Used by (from the same schema document) | Complex Type CreditDefaultSwap |

| Abstract | no |

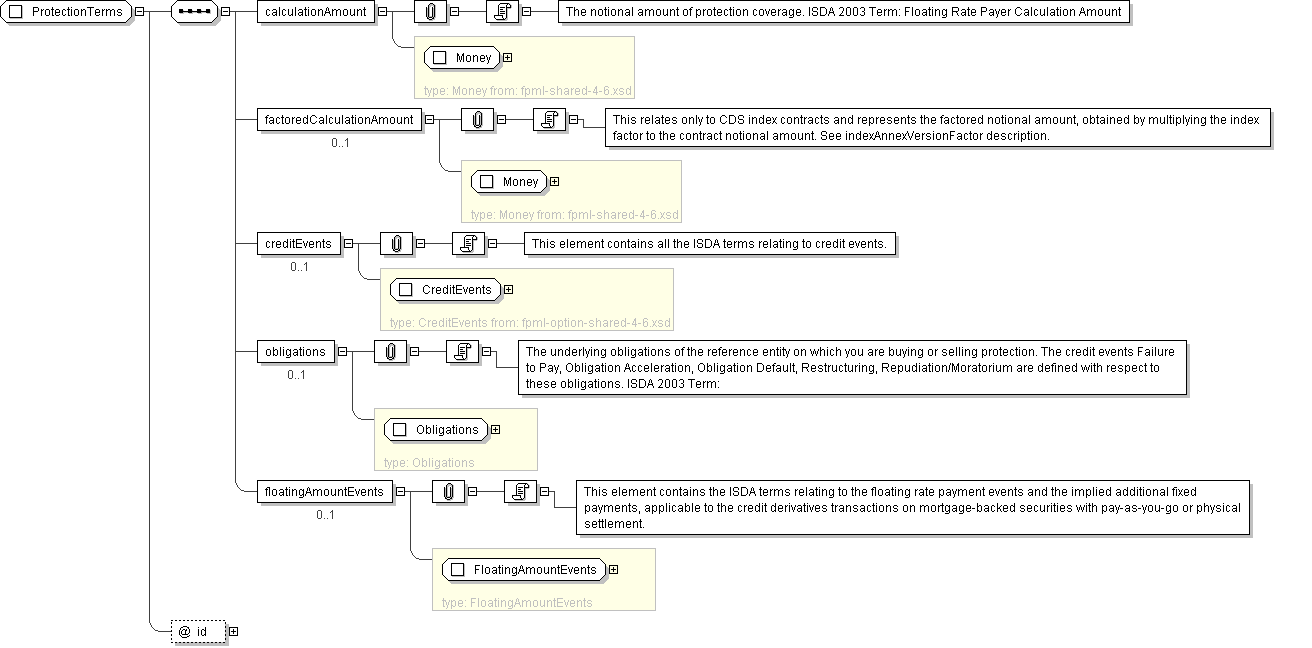

'The notional amount of protection coverage. ISDA 2003 Term: Floating Rate Payer Calculation Amount'

'This relates only to CDS index contracts and represents the factored notional amount, obtained by multiplying the index factor to the contract notional amount. See indexAnnexVersionFactor description.'

'This element contains all the ISDA terms relating to credit events.'

'The underlying obligations of the reference entity on which you are buying or selling protection. The credit events Failure to Pay, Obligation Acceleration, Obligation Default, Restructuring, Repudiation/Moratorium are defined with respect to these obligations. ISDA 2003 Term:'

'This element contains the ISDA terms relating to the floating rate payment events and the implied additional fixed payments, applicable to the credit derivatives transactions on mortgage-backed securities with pay-as-you-go or physical settlement.'